Managing your personal finances is a bit like steering a ship—it’s easier with calm seas and a steady wind. But when your pay schedule shifts, it can feel like someone just threw you into a storm without a compass. Whether you’ve moved from weekly to bi-weekly pay, taken on freelance gigs with unpredictable income, or are adjusting to a new job with a different compensation structure, it’s easy to feel disoriented. The good news? With a bit of preparation and smart strategies, you can stay on course and even thrive amid the change.

Let’s explore how to regain control and create a flexible financial plan that works—no matter how often (or irregularly) you get paid.

Understanding the Financial Ripple Effects

A change in how and when you’re paid doesn’t just affect your wallet—it impacts your entire financial routine. Suddenly, your bills might not sync with your income. You may find yourself leaning more on credit to bridge the gap between paychecks. And if your income varies in amount as well as frequency, it becomes even more difficult to plan ahead.

Here’s how a changing pay schedule can disrupt your finances:

- Bill Timing Mismatches: Monthly bills don’t care if your paycheck is delayed.

- Cash Flow Droughts: Gaps between paychecks can lead to overspending when funds do finally arrive.

- Income Volatility: Commission-based or freelance pay can create stress if you don’t have a reliable backup.

Recognizing these issues early helps you plan proactively instead of reacting under pressure.

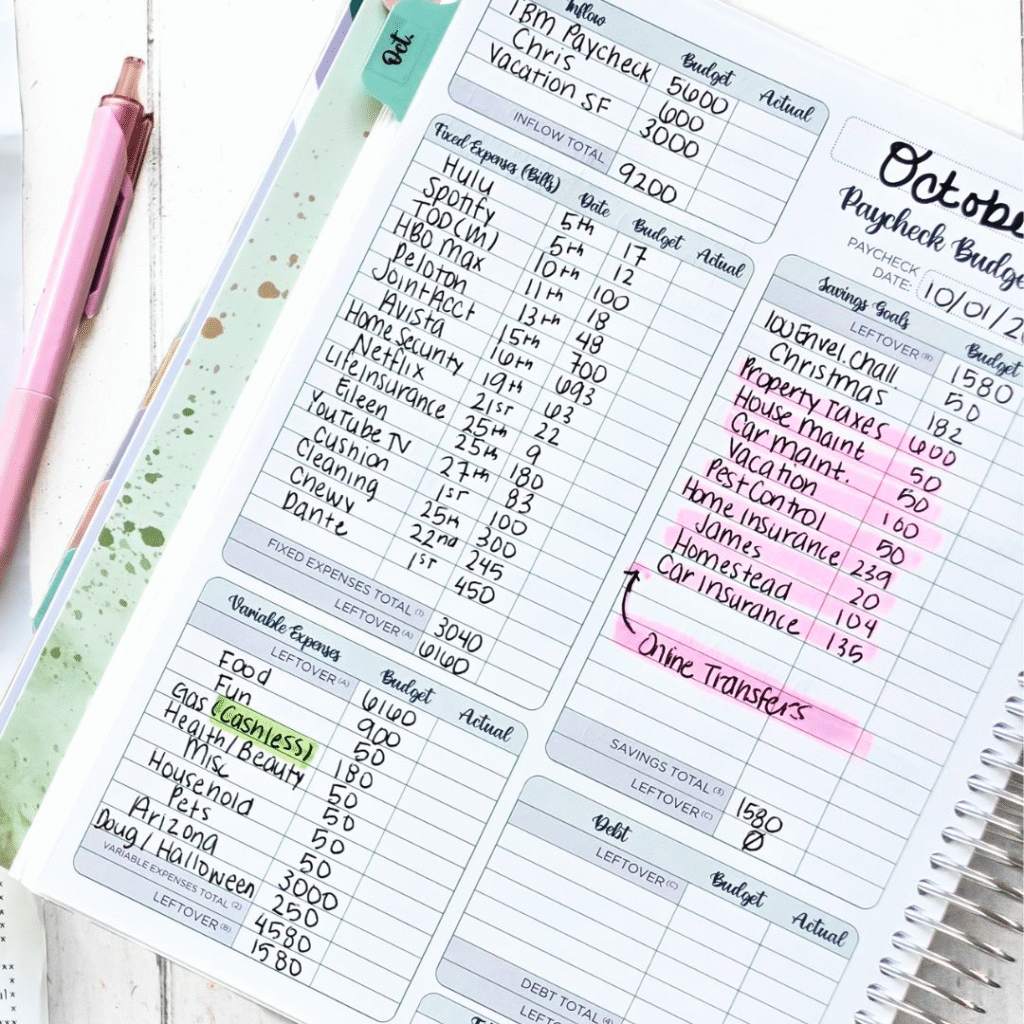

Build Your Financial Cushion

One of the most powerful tools for regaining stability is a financial buffer. Think of it as a safety net in your checking account—money that’s always there to help smooth over those unpredictable bumps.

Start small if you have to. Set aside $50 to $100 from each paycheck, and aim to build up to a comfortable amount (many people target around $1,000). This buffer lets you:

- Cover bills before your next paycheck hits

- Avoid reaching for credit cards during shortfalls

- Handle small emergencies without panic

Automating this process is key. If your bank allows it, schedule a recurring transfer to your buffer every payday. Over time, this small habit builds a big sense of security.

Use Sinking Funds to Stay Prepared

When your income is less predictable, it becomes even more important to plan for future expenses in bite-sized chunks. That’s where sinking funds come in.

Instead of scrambling to cover a big cost (like annual insurance premiums or holiday gifts), sinking funds let you break those expenses into manageable pieces. Here’s how:

- Name the Expense: Pick what you’re saving for—car repairs, back-to-school shopping, a vacation.

- Calculate the Total: Estimate how much you’ll need.

- Set a Deadline: Decide when you’ll need the money.

- Divide and Conquer: Break that total into portions based on how many pay periods remain.

For example, saving $500 over 10 paychecks just means setting aside $50 each time. Track your progress with a simple spreadsheet or budgeting app so you can see where your money’s going.

Align Your Bills with Your Paydays

One often-overlooked solution is adjusting your bill due dates to better match your income schedule. Most utility companies, credit card issuers, and lenders will let you choose a due date that works better for you—especially if you explain your new situation.

Once your bills line up with your pay schedule:

- Set up automatic payments to avoid missed due dates.

- Prioritize essentials—housing, utilities, transportation—especially if funds are tight between paydays.

This simple step can significantly reduce late fees, stress, and the temptation to dip into credit.

Master Variable Spending

When your income fluctuates, variable expenses—like groceries, entertainment, or dining out—can throw your entire budget off balance.

Here are a few practical ways to rein in this spending:

- Use the cash envelope method: Whether you prefer physical envelopes or digital tools, allocate fixed amounts for categories like groceries, gas, or fun money. When the envelope is empty, the spending stops.

- Meal plan to avoid grocery overspending: Plan meals around what you already have at home. Make a list before shopping to avoid impulse buys.

- Trim discretionary expenses temporarily: Cut streaming subscriptions, limit eating out, or find free entertainment alternatives during tighter months.

These small adjustments can make a big difference when you’re waiting for that next paycheck to land.

Reevaluate Your Emergency Fund

Your emergency fund is your financial lifeline during true crises—job loss, medical emergencies, or other unexpected events. With a more irregular pay schedule, the importance of this fund increases tenfold.

Ideally, aim to build 3–6 months’ worth of living expenses. That might sound daunting, but remember, you can:

- Automate your savings: Just like a bill, treat it as non-negotiable.

- Cut non-essentials: Pause unnecessary spending until you reach your goal.

Even slow progress is still progress—and every dollar saved adds to your peace of mind.

Stay Agile: Regular Budget Check-Ins

When your income changes, your budget needs to change too. One of the best habits you can build is to review your finances at least once a month.

Ask yourself:

- Are you consistently overspending in certain areas?

- Did any unexpected expenses come up?

- Are your sinking funds and emergency savings still on track?

Adjust categories, shuffle priorities, and keep the lines of communication open with yourself (and your family, if applicable). Financial flexibility isn’t just helpful—it’s essential when your paychecks vary.

Final Thoughts

Life isn’t static, and neither is your income. But with proactive planning, thoughtful saving, and a willingness to adapt, you can stay financially stable even when your pay schedule changes.

Think of your budget as a living tool, not a rigid rulebook. The more you tailor it to fit your current reality, the more confident and in control you’ll feel—no matter when payday comes around.

Would you like a printable checklist or worksheet to help manage this process more easily?

{kind=link}