Let’s face it—life rarely goes as planned. One minute you’re cruising through your budget, and the next, your car breaks down, your kid needs braces, or you get hit with an unexpected layoff. That’s why budgeting can’t just be about numbers on a spreadsheet or perfect monthly categories. It needs to work in the chaos, not just the calm.

Hi, I’m Miko. After digging myself out of $77,000 in debt as a single mom earning just $30,000 a year, I made it my mission to help others take control of their finances through realistic, sustainable strategies. At The Budget Mom, I’ve taught millions how to manage their money with compassion, flexibility, and confidence—even when life is far from perfect.

If your budget always seems to collapse under the weight of real life, here’s how to create one that bends but doesn’t break.

1. Budget for the Life You Actually Live

Many people fall into the trap of creating an “ideal” budget—one that reflects the life they wish they had rather than the one they’re living. But hope isn’t a strategy, and pretending doesn’t pay the bills.

Start by looking at your current reality:

- How much money do you actually bring in each month (wages, side hustles, support)?

- Where does your money truly go—on paper, not in your head?

- What debts and obligations are non-negotiable?

- What surprise expenses seem to “sneak up” on you every year?

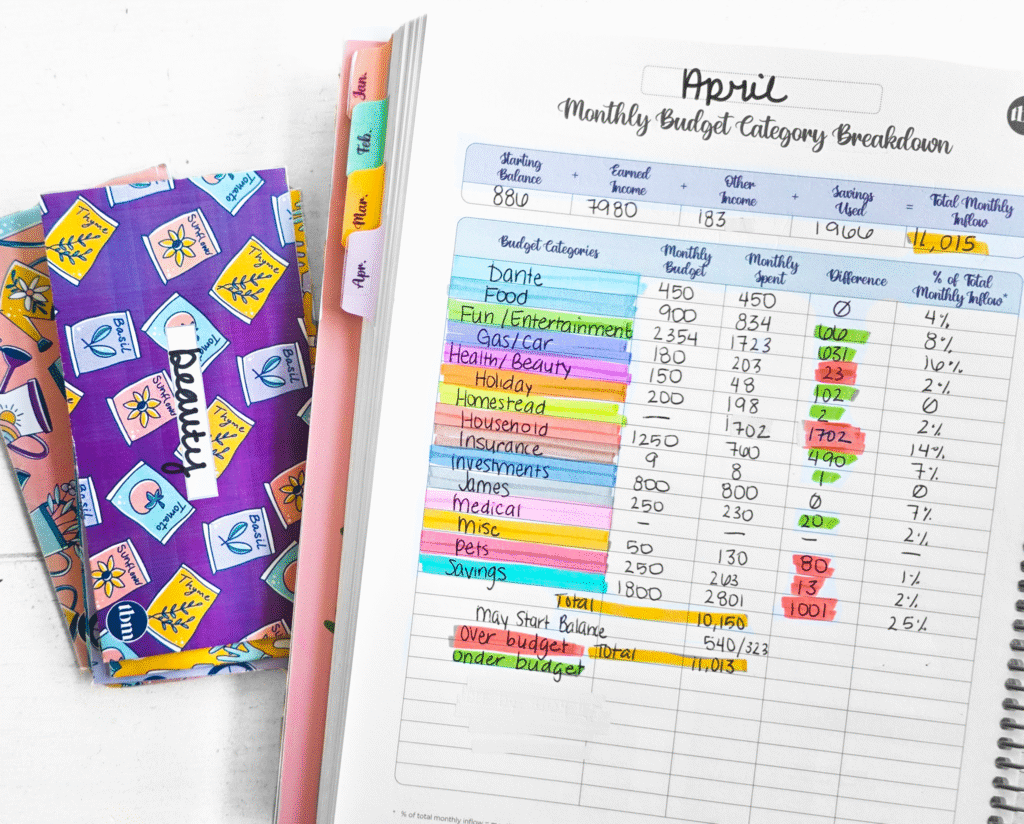

Grab your latest bank and credit card statements and highlight every single transaction. Group them by category. This simple, honest exercise lays the foundation for a realistic, responsive budget—what I call the Budget by Paycheck Method.

2. Design for Flexibility, Not Perfection

Budgets that break under pressure are usually too rigid. Think of it like building with Jenga blocks—one unexpected shake and the whole thing crashes.

Real-life budgets need room to breathe:

- Add a buffer line item, like “miscellaneous,” to catch unplanned expenses.

- Set up sinking funds for predictable-but-irregular costs (car repairs, holidays, pet care).

- Don’t overcomplicate your categories. Simpler budgets are often more sustainable.

Remember, it’s better to build margin than to micromanage.

3. Make It Personal, Not Picture-Perfect

No two financial journeys look the same—and that’s okay. Your budget should reflect your current phase of life and your unique priorities.

- In survival mode? Go minimalist and focus on essentials.

- Recovering from hardship? Carve out space for healing—whether that’s therapy, rest, or small joys.

- Working to grow? Invest in your future self through education, savings, or business tools.

Perfection isn’t the goal—personalization is.

4. Budget By Paycheck, Not By Calendar

Traditional monthly budgeting assumes your bills and paychecks align neatly. But real life doesn’t work that way. That’s why I teach budgeting by paycheck.

Here’s how:

- List all expenses due before your next paycheck.

- Allocate just that paycheck to cover those specific costs.

- Repeat for each pay period.

This method helps you avoid running out of money mid-month and makes planning far more intuitive.

5. Give Every Dollar a Job—But Keep It Flexible

Being intentional with your money means assigning a job to every dollar. But those jobs don’t have to be fixed in stone.

Example: You budgeted $200 for groceries but spent only $150. That leftover $50? That’s not a mistake—it’s freedom. Move it to savings, cover a surprise bill, or pad a sinking fund. Budgeting should adapt, not restrict.

6. Progress Over Perfection

Even now, after years of budgeting, I don’t hit my numbers perfectly. And I don’t expect you to either.

The real goal? Awareness and intention.

Did you make better choices than last month? Did you catch a spending habit early? Did you have cash set aside when an emergency popped up?

Those are wins. Celebrate them.

7. Make Adjustments—Budgeting Isn’t “Set and Forget”

Life changes. So should your budget.

At the end of each month, do a quick reflection:

- What went smoothly?

- Where did you feel the squeeze?

- What unexpected costs came up?

- What do you want to try differently next month?

This simple review process helps you learn and grow—and ensures your budget evolves with you.

8. Address the Emotions Behind the Numbers

Money isn’t just math. It’s deeply emotional.

Maybe your budget keeps breaking because you’re carrying guilt, shame, or fear around money. Maybe you were never taught how to manage it, or maybe you’re trying to unlearn years of financial anxiety.

You’re not failing. You’re human.

What you need isn’t more willpower—it’s more compassion.

9. Build a System, Not Just a Spreadsheet

You don’t need fancy apps or color-coded perfection. You need a system that matches your real income, your real priorities, and your real life.

That’s why I created the Budget by Paycheck Method. It walks you through every part of the process—from planning and tracking to reflecting and adjusting.

It works because it’s designed for the messiness of life.

Final Thoughts: Budget Like a Real Person

Life is unpredictable. Your budget doesn’t need to be flawless to be effective—it just needs to work for you.

When you create a budget that’s grounded in your reality, built to flex with change, and rooted in your values, it becomes more than a financial tool—it becomes a guide to confidence, peace, and freedom.

So let go of perfection. Embrace what’s possible. And budget like a real person living a real life.

That’s the kind of budgeting that actually works.

{kind=link}